50/30/20 Rule: Is It Still Effective in Today’s Economy?

The 50/30/20 rule has long been a go-to budgeting method for managing personal finances. Its simplicity and structure have helped millions build better money habits. But in today’s rapidly changing economy—marked by rising living costs, student debt, and income instability—many are asking:

Is the 50/30/20 rule still relevant?

In this article, we’ll break down how the rule works, its advantages, modern challenges, and whether it still fits today’s financial reality. We’ll also explore updated strategies and alternatives to help you stay financially secure.

What Is the 50/30/20 Rule?

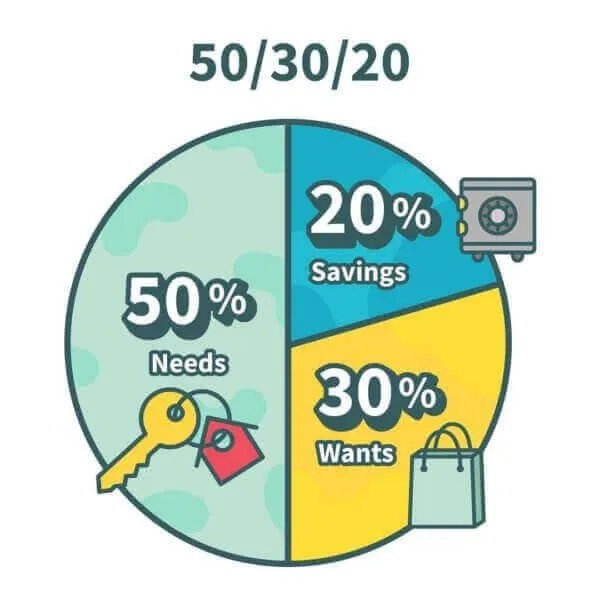

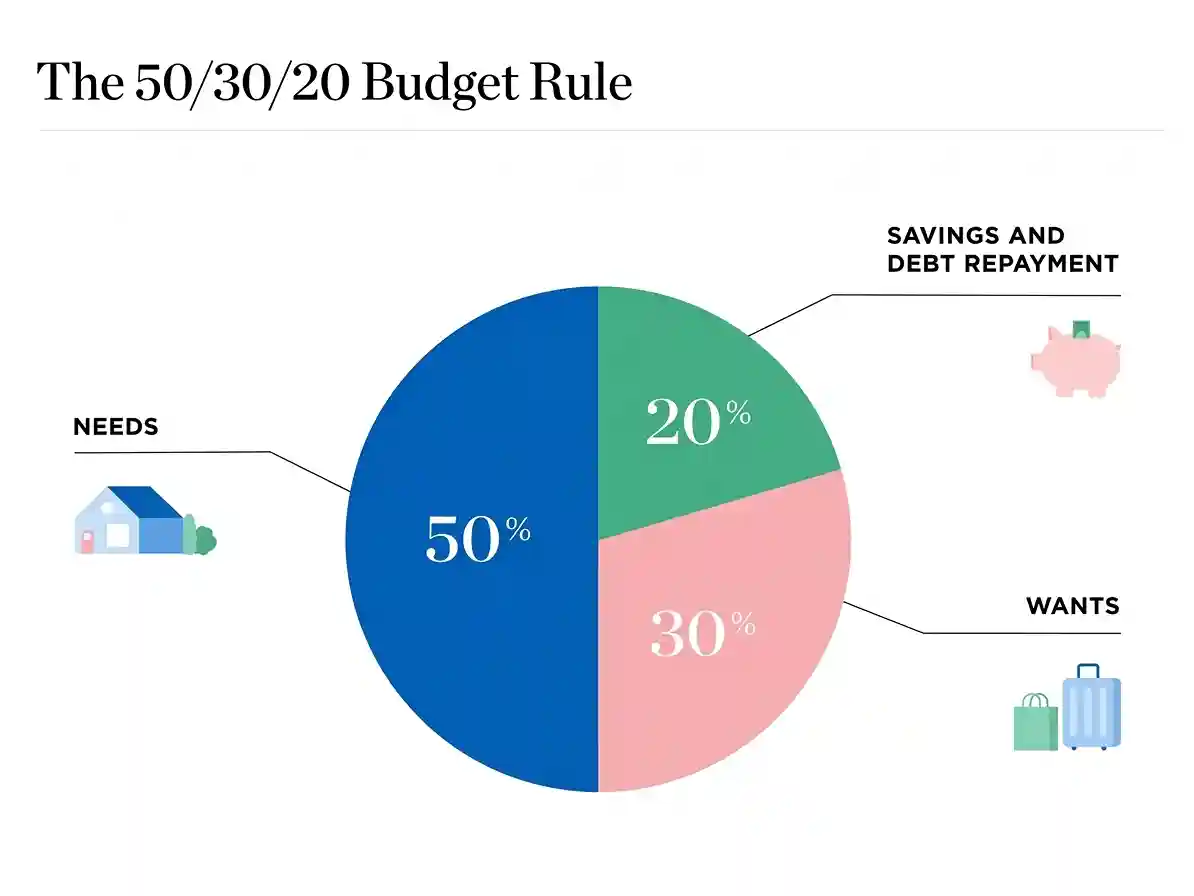

The 50/30/20 rule is a simple budgeting framework that divides your after-tax income into three categories:

- 50% for Needs

Essential expenses like housing, groceries, utilities, healthcare, and transportation. - 30% for Wants

Non-essential spending such as dining out, entertainment, travel, and hobbies. - 20% for Savings and Debt Repayment

Includes emergency funds, retirement savings, investments, and paying off debt.

This method is popular because it offers a clear and balanced approach to managing money without requiring complex calculations.

Why the 50/30/20 Rule Still Works

Despite economic changes, the 50/30/20 rule continues to offer several key benefits:

1. Simplicity and Accessibility

It’s easy to understand and implement, even for beginners with no financial background.

2. Encourages Financial Discipline

By assigning clear spending limits, it helps prevent overspending and promotes mindful money management.

3. Built-In Flexibility

Although the percentages are guidelines, they can be adjusted based on individual circumstances.

4. Promotes Long-Term Financial Security

The 20% savings allocation encourages consistent saving and debt reduction, helping build wealth over time.

Challenges in Today’s Economy

While the rule is effective in theory, modern financial realities can make it harder to follow.

Rising Cost of Living

Housing, healthcare, and education costs have increased significantly. In many cities, rent alone can exceed 50% of income.

Student Debt Burden

Many young professionals carry large student loans, reducing their ability to save or spend freely.

Income Instability

Freelancing, gig work, and contract jobs create unpredictable income, making fixed percentages difficult to maintain.

Technology and Lifestyle Costs

Internet, software, and digital tools are now essential expenses that didn’t exist when the rule was created.

How Millennials and Gen Z Can Adapt the Rule

Younger generations face unique financial challenges, but the 50/30/20 rule can still work—with adjustments.

Customize Your Percentages

Instead of strictly following 50/30/20, consider:

- 60/20/20 if living costs are high

- 50/20/30 if prioritizing savings

Focus on Flexibility

Regularly adjust your budget based on income changes, career growth, or life events.

Use Budgeting Apps

Digital tools can help track spending, categorize expenses, and automate savings.

Align Spending With Values

Many younger individuals prioritize experiences, education, and personal growth—your budget should reflect that.

Modern Alternatives to the 50/30/20 Rule

If the traditional method doesn’t fit your lifestyle, here are some effective alternatives:

Zero-Based Budgeting

Every dollar is assigned a purpose, ensuring complete control over your finances.

Pay Yourself First

Prioritize saving and investing before covering expenses—ideal for building wealth faster.

Envelope System

Use cash for different categories to limit overspending.

70/20/10 Rule

- 70% for expenses

- 20% for savings

- 10% for investments

This approach works well for those focused on aggressive financial growth.

What Financial Experts Say

Many financial experts agree that the 50/30/20 rule is still useful—but not perfect.

- Some view it as a great starting point for beginners

- Others emphasize the need for customization based on individual circumstances

- Critics argue that its simplicity may overlook modern financial complexities

The consensus?

The rule works best when combined with financial education and flexibility.

Final Verdict: Is the 50/30/20 Rule Still Effective?

Yes—but with a caveat.

The 50/30/20 rule remains a powerful foundation for budgeting, especially for those new to personal finance. However, in today’s economy, it should be treated as a flexible guideline rather than a strict formula.

Key Takeaways:

- Use the rule as a starting framework

- Adjust percentages to match your reality

- Stay consistent with saving and tracking

- Combine it with modern tools and strategies

Conclusion: Build a Budget That Works for You

There’s no one-size-fits-all solution in personal finance. The best budget is the one you can stick to consistently.