How Much of Your Income Should You Be Investing? Experts Recommend 15%

One of the first questions people often ask when planning for their financial future is: “How much of my income should I invest?”

If you’re asking this, congratulations—you’re already thinking ahead. Investing isn’t just a way to grow your wealth; it’s a crucial step toward building financial security and ensuring a comfortable retirement. The good news? You don’t need a large sum to get started. What matters most is consistency and discipline, so that your money has time to compound and grow over the long term.

Why Investing Early Matters

Starting to invest early in your career gives your money more time to work for you. Thanks to the power of compound interest, even small contributions can grow substantially over decades. For example, investing $200 a month starting at age 25 could result in over $300,000 by age 65, assuming a moderate annual return of 7%.

The key takeaway is simple: the earlier you start, the easier it is to reach your financial goals.

The Expert-Recommended Investment Percentage

Financial experts generally recommend allocating around 15% of your pretax income toward investments. This percentage strikes a balance between growing your retirement fund and covering current expenses.

Matt Rogers, a CFP and Director of Financial Planning at eMoney Advisor, suggests using the 50/15/5 rule as a practical guide for managing income.

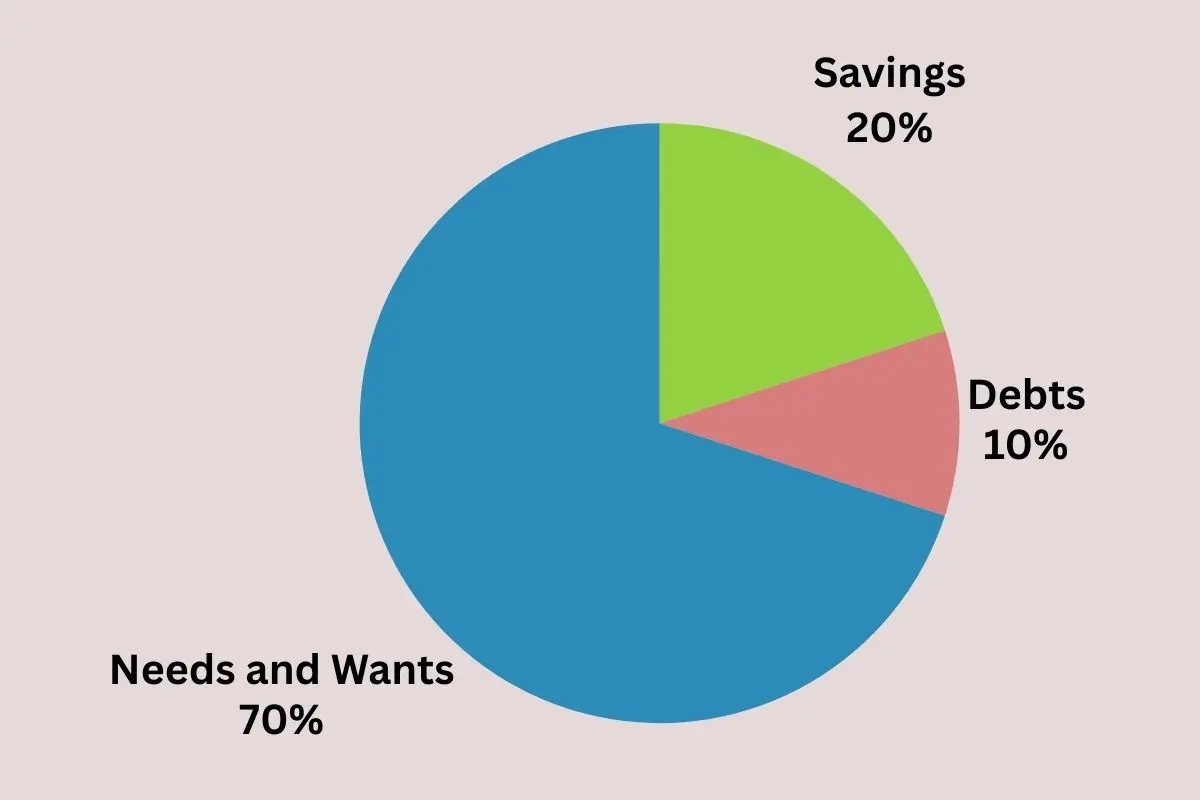

Understanding the 50/15/5 Rule

Here’s how it breaks down:

- 50% of your take-home pay should go to essential living expenses: housing, groceries, healthcare, transportation, childcare, and debt repayment.

- 15% of pretax income (including any employer contributions) should be allocated to long-term investments for retirement.

- 5% of take-home pay should be saved for short-term goals or emergencies, such as an emergency fund or unexpected medical costs.

This leaves 30% of your income for discretionary spending—things like dining out, travel, hobbies, or even additional savings and investment contributions.

By following this approach, you maintain a healthy balance between enjoying today’s lifestyle and planning for tomorrow’s financial security.

How to Start Reaching the 15% Goal

The 15% rule assumes you start investing early, but it can feel challenging for young professionals or those with limited income. Here are some practical tips:

- Maximize Employer 401(k) Matches

If your company offers a 401(k) match, contribute at least enough to get the full match. This is essentially free money for your retirement and a great first step toward the 15% goal. - Increase Contributions Gradually

If you can’t immediately invest 15% of your income, start small. Increase your contributions by 1–2% each year or whenever you get a raise. Over time, these small increases compound into a significant difference. - Automate Your Investments

Setting up automatic transfers to your retirement or investment accounts ensures that you stick to your plan and removes the temptation to spend the money elsewhere. - Use Online Tools

Tools like Fidelity’s Savings and Spending Calculator can help you track your progress, compare your budget to the 50/15/5 guideline, and see exactly how much you can invest each month.

Adjusting for Life Changes

Life is unpredictable, and your financial plan should be flexible. Events such as a job change, a new child, or buying a home may temporarily affect how much you can invest. The important thing is to get back on track as soon as possible and continue contributing regularly. Even small amounts make a difference over time.

Final Thoughts

Investing 15% of your pretax income is a practical guideline for most people. By following the 50/15/5 rule, taking advantage of employer contributions, and gradually increasing your investment over time, you can grow your wealth steadily while maintaining financial stability in the present.

Remember: starting today is better than waiting for the “perfect” time. Even modest contributions now can grow into a substantial retirement nest egg decades later.