Achieving financial freedom by 30 might sound ambitious, but it’s far more realistic than most people think. You don’t need a six-figure salary or extreme frugality to get there. What you do need is a clear plan, smart financial habits, and consistent execution.

In this guide, you’ll learn 10 practical steps to achieve financial freedom by 30, even if you’re just starting your financial journey.

What Does Financial Freedom by 30 Really Mean?

Before diving into strategies, it’s important to define your goal.

For some people, financial freedom means:

- Having enough savings to cover emergencies

- Being debt-free

- Generating passive income

- Not relying entirely on a paycheck

👉 The clearer your definition, the easier it is to create a plan and stay motivated.

define-your-financial-goals-clearly

Start by identifying what you want financially by age 30.

Ask yourself:

- How much do I want to save?

- Do I want to be debt-free?

- Do I want passive income?

Clear goals give direction and help you measure progress toward financial independence.

Start by identifying your financial targets for the next few years. Ask yourself:

- How much do I want to save by 30?

- Do I want to eliminate all debt?

- How much passive income do I need?

Clear and specific goals give you direction and help measure your progress toward financial independence.

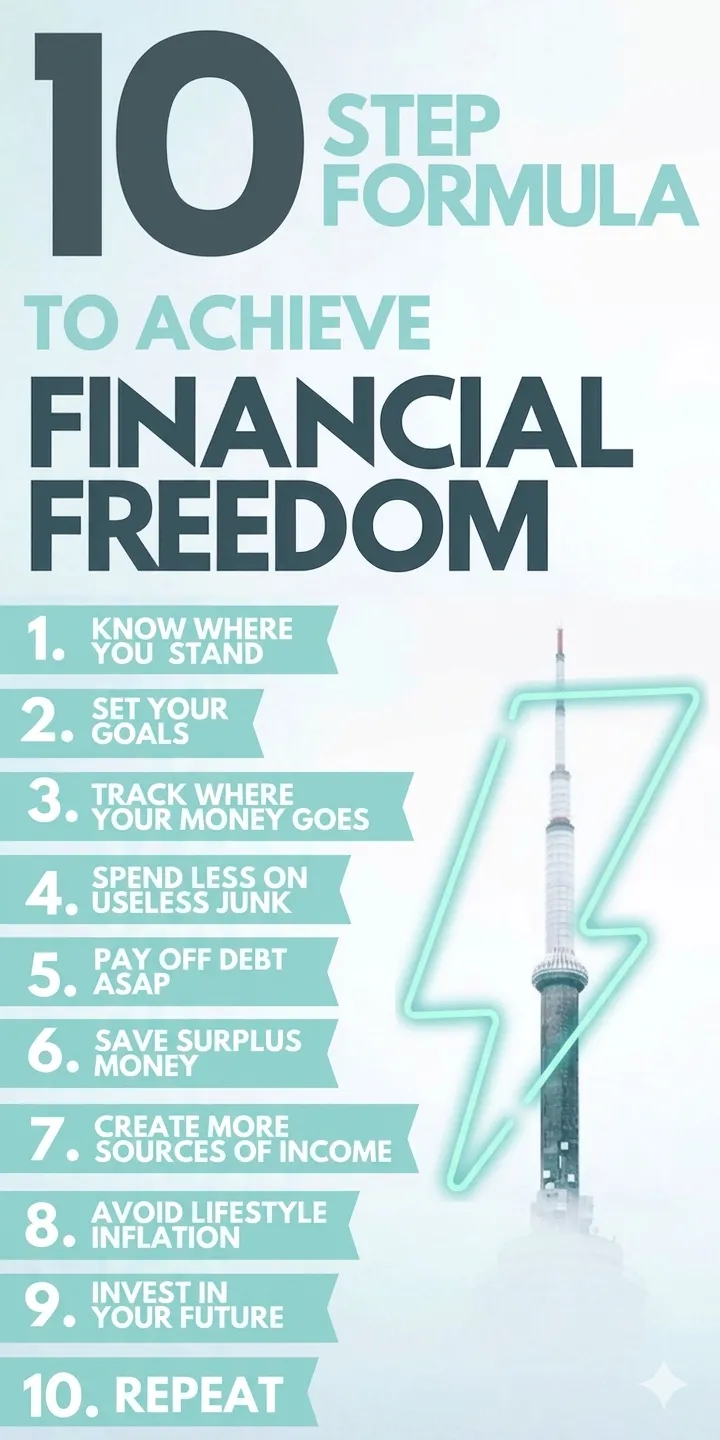

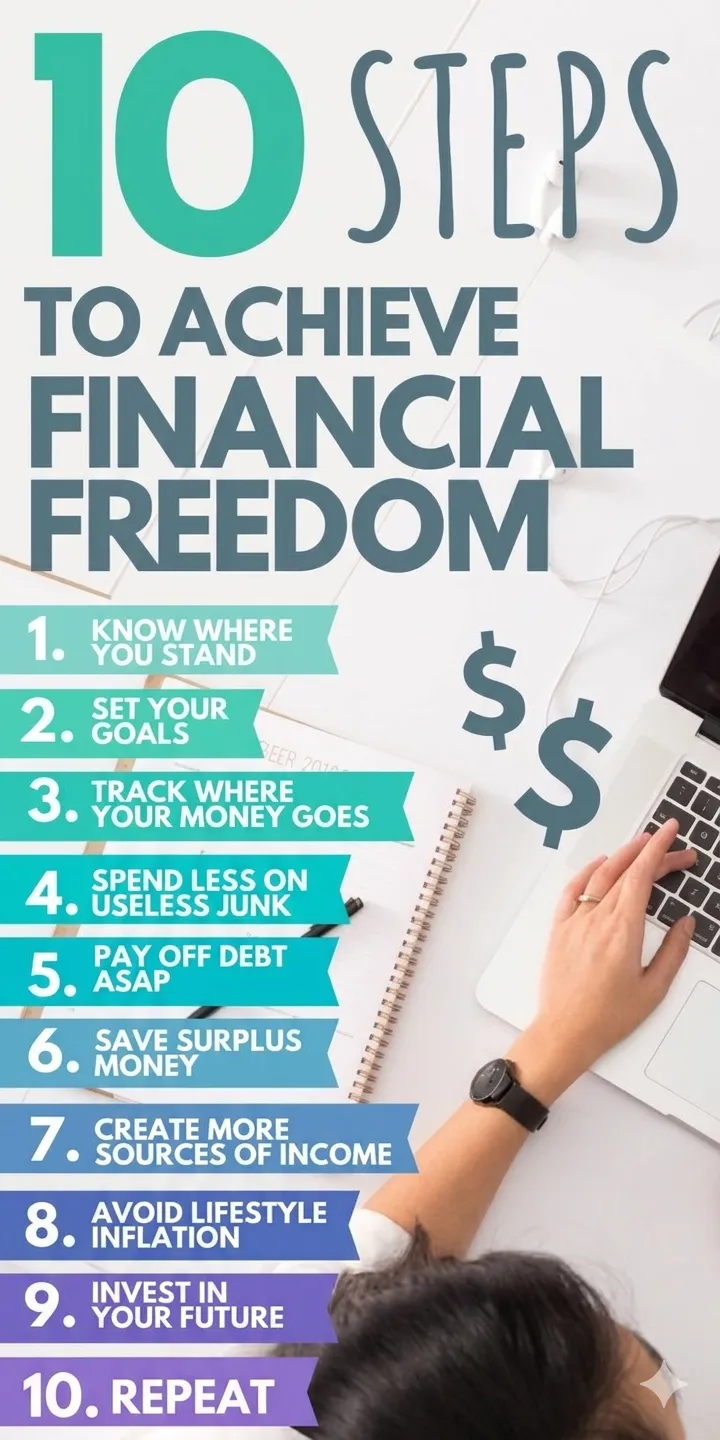

- Track and Control Your Spending

Many people underestimate how much they spend daily.

Track every expense, including:

- Coffee and snacks

- Subscriptions

- Entertainment

👉 Use budgeting apps or spreadsheets to monitor your spending.

Once you understand where your money goes, you can cut unnecessary expenses and redirect funds toward savings and investments.

- Live Below Your Means

This is one of the most important habits for building wealth.

Even if your income increases:

- Avoid upgrading your lifestyle too quickly

- Keep expenses lower than your earnings

👉 The gap between what you earn and what you spend is what builds wealth.

- Avoid Unnecessary Debt

Not all debt is bad—but high-interest consumer debt is dangerous.

Avoid:

- Credit card debt for lifestyle spending

- Loans for non-essential purchases

👉 Focus on paying off existing debt quickly to free up cash for saving and investing.

5. Set Small, Achievable Milestones

Big financial goals can feel overwhelming. Break them down into smaller steps:

- Save $500 in 1–2 months

- Pay off a specific debt in 6 months

- Build a $1,000 emergency fund

👉 Small wins create momentum and keep you motivated.

- Improve Your Financial Literacy

Knowledge is a powerful advantage.

Learn about:

- Budgeting

- Investing

- Personal finance strategies

👉 Read books, follow financial blogs, and learn from trusted experts. The better you understand money, the better decisions you’ll make.

- Start Investing Early

Time is your biggest asset when it comes to investing.

Even small amounts can grow significantly through compound interest.

Begin with:

- Index funds (e.g., S&P 500)

- ETFs

- Long-term stock investments

👉 Consistency matters more than starting big.

- Automate Your Savings

Make saving effortless by automating it.

Set up:

- Automatic transfers to savings accounts

- Monthly investment contributions

👉 This “pay yourself first” strategy ensures you stay consistent without relying on willpower.

- Take Advantage of Employer Benefits

If your employer offers retirement contributions or matching:

👉 Use it.

This is essentially free money that:

- Boosts your savings

- Accelerates wealth building

Even small contributions can grow significantly over time.

- Take Smart, Calculated Risks

Building wealth often requires stepping out of your comfort zone.

Examples include:

- Starting a side hustle

- Switching to a higher-paying job

- Investing in new opportunities

👉 The key is to take calculated risks, not reckless ones.

Finding the Right Balance

Financial freedom doesn’t mean you stop enjoying life.

Instead, aim for balance:

- Spend on things that truly matter

- Cut what doesn’t add value

- Save and invest consistently

👉 You can enjoy today while still building a secure future.